Remsenburg-Speonk School District Mismanaged Fund Balance, Audit Finds

Remsenburg-Speonk Union Free School District’s Board of Education and officials did not properly manage its fund balance over a five-year span, auditors with the New York State Comptroller Thomas DiNapoli’s office found.

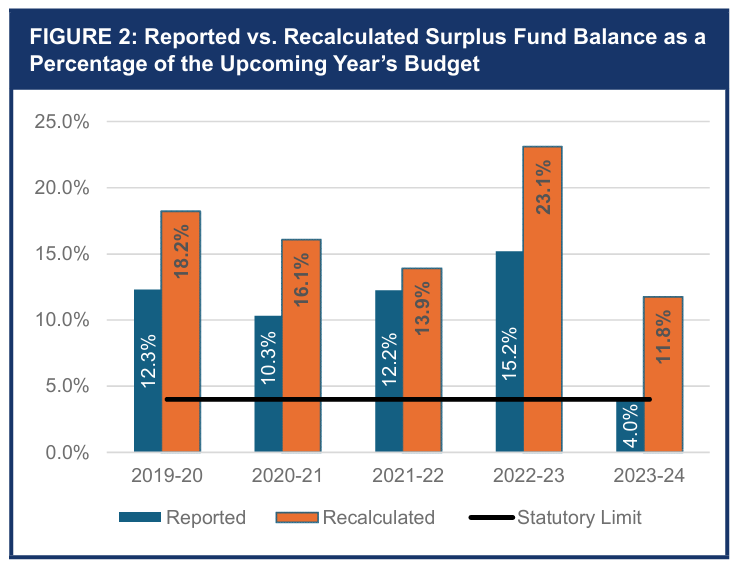

A district’s fund balance is the difference between revenues and expenditures over a period of time. When there is a surplus fund balance, they are allowed to retain a portion of it up to four percent of the budget.

“The board appropriated surplus fund balance, in part, because it adopted budgets that annually overestimated appropriations by an average of $1.3 million (9%) per year, or a cumulative total of approximately $6.4 million,” the auditors stated in their 12-page report released on July 18. “The majority of the overestimated appropriations ($5.6 million) were for special education instruction.”

Between fiscal years 2019-20 and 2022-23, the district recorded a surplus fund balance between 10 and 15%. Over the last five years, they appropriated a $5.5 million surplus fund balance but used only $350,000 of that amount, meaning that “when the unused appropriated fund balance is added back to the district’s reported surplus fund balance, the recalculated amount ranged from approximately 12 to 23% of the upcoming year’s budget.”

In a written response, Remsenburg-Speonk Superintendent Denise Lindsay-Sullivan said the district plans to implement three of the comptroller’s recommendations and support for a law that would allow school districts to establish a reserve fund for special education expenses.

“Such a reserve fund could offer financial resilience, reducing year-to-year volatility and allow districts to have less fluctuation from year-to-year, while eliminating the need to overestimate for special education instruction,” she wrote. “The cost of educating high-needs students is comparable across districts, but for a small district like ours, these expenses represent a significantly larger portion of our overall budget…”

The district has 90 days to present a written corrective action plan to the comptroller’s office.

Vetted Hamptons Resources